Righto, two things. (1) Iâ’ve given myself half an hour to race through this and (2) I’m very sorry about the pun. Terry’s idea. With both of these in mind, let’s move swiftly on.

Embark finally announced its long-awaited charging structure the other day and you know the drill by now, we’ve got your back on this. Time to dust the stoor off the lang cat pricing engine and see how competitive it looks. *SPOILER ALERT* Very.

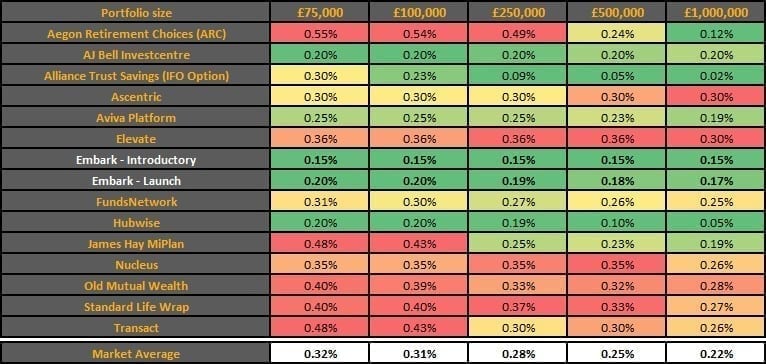

First things first, here’s the skinny on how it shapes up:

- It’s a tiered %-based arrangement, with differentiated charges for pension compared to ISA/GIA. Third-party admin is cheaper still.

- For an introductory period, customers will pay 0.25% tiering down to 0.15% for pension and 0.15% across the piece for the other wrappers. This offer is open until the end of next year and is then locked in for the lifetime of the investment. Nice.

- After that, the pension will cost 0.275%, tiering down to 0.20%, while ISA/GIA will start at 0.20% and drift effortlessly down to 0.15%.

- Fund trading/rebalancing is free. Stockbroking charges are 0.07% a trade (so buy or sell) with a £7.50 min and £120 max, or £1 per rebalance within a model.

25 minutes to go. Jings. Pension table first. Custody and wrapper costs only here. No trading activity. Two lines for Embark, one for the introductory rate and one for the! Oh. You figured it out. Cool.

One last thing to point out before we get to the colouring book. These tables are a subset of our full peer group and AUA points. Subscribers to our stuff get access to the full gig.

ISA/GIA now. Same rules as the pension table

And now a mixed wrapper portfolio (50% pension, 25% ISA, 25% GIA) with a 10-fund model portfolio that rebalances quarterly. Your mileage will vary[1].

Lots to say and my entirely artificial clock is ticking. Here are the headlines:

- You only need to glance at the colouring of the table (that is kind of the point) to see how competitive the Embark structure is. It’s green everywhere in the tables here and only starts to fade at the higher AUA points in our full tables

- Embark has openly stated that it is targeting a core market of between £25k and £150k so from a competitive standpoint, it’s bang on the money here.

- Extending that point a wee bit, average on-platform pot sizes are smaller than many might think. Take away the outliers (those with a SIPP specialist heritage and those who specifically target HNW) and your mode average is something-not-that-much-higher-than[2] £100k or so.

- So, for a £100k mixed portfolio, pretty much the platform market centre of gravity, Embark is around half the market rate. Not just a few basis points. Half the market rate.

- Our tables look at fund investment only (because our research shows that 94% of on-platform assets are held in cash and collectives). Were we to assume an element of equity investment within a portfolio, then this picture would change.

It’s been a funny old time in platform pricing over the past year or so. Lots of activity but in different directions, the net result of which has been ‘much of a muchness’ in terms of market rate. Until now that is. Embark, along with other noob, Hubwise, is threatening to shake things up a bit and redefine our perception of the market rate.

We expect further market activity in the next wee while. An obvious example is Aegon and Cofunds post conscious-coupling. Their initial rates of 0.60% and 0.29% respectively are clearly incompatible, not to mention the fact that Aegon has been extremely vocal about scale driving down costs.

The FCA’s Investment Platforms Market Study and its quest to assess competition and value for money lurks in the hinterland alongside all of this. You can’t escape the feeling that these pricing structures will excuse Embark from most of the awkward conversations. In fact, they may well have kicked off a few more elsewhere.

One minute to go. Just enough time for a shameless punt of our stuff. We put out our annual platform guide the other week complete with comprehensive pricing analysis. Embark just missed the cut on this but if you’d like updated tables, give me a shout.

[1] Based on our quarterly platform research, this is a representative wrapper split. Obviously, each client is a special snowflake and will have their own split.

[2] #science.