Hi folks, it’s yours truly, Rich Mayor at the TCWU helm this week, which means it’s time to have a little look at how last quarter went and, hopefully, a brief distraction from just HOW DAMN HOT it is. We’re tantalisingly close to being able to share what’s happened on an individual basis at platforms in Q2 2022, but until then (tomorrow), here’s a little snippet into some of the stuff we’ve spotted at an aggregated level.

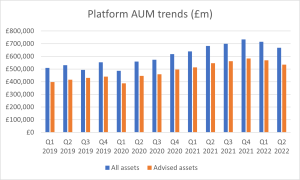

First up is asset growth, or indeed lack thereof, for the platform market. It’s not all that often we pick up the red pen for year-on-year comparisons for asset growth (though we did during the pandemic), but in some rather choppy markets asset growth for all channels and the advised channel are down a couple percent on this time last year. Pretty astonishing that we’ve gone from a year of record-breaking sales in 2021 to negative asset growth year-on-year but, alas, here we are.

In the advised world, on top of last quarter’s falls in assets, we’ve seen more than £48bn wiped off since the end of last year (about the size of advised assets at Transact or Fidelity Adviser Solutions last quarter). Naturally, a fall in value results in lower ongoing charges and fee revenues for platforms and advisers, and you might be forgiven for thinking that sales numbers are going to be pretty awful, but they definitely were not.

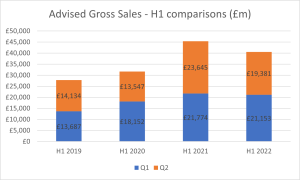

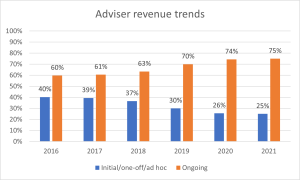

Though down on the same record-breaking quarters last year, sales are comfortably above pre-pandemic levels, which is perhaps the closest we can get to examining apples with other apples. When we look at first half of the year comparisons, the performance in 2022 in these markets has shown some strong resilience. Advisers we’ve spoken to say that they’ve, very sensibly and understandably, been spending more time reassuring clients and reviewing financial plans that might have changed due to *gestures at broadly everything in the UK at the moment*. It makes even more sense when we look at recently released FCA data which shows ongoing fees form around three quarters of adviser revenue now, up a smidge on the previous year. One suspects platforms will also be looking after their biggest supporters too.

Source: https://www.fca.org.uk/data/retail-intermediary-market-2021

We’ll leave net sales findings for the wider publication (the story is similar to gross sales) and coming full circle to asset growth. Margins at platforms have been historically wafer-thin and platform charges have only gone down, so we’ve seen some branching out over the last decade into other revenue-generating avenues, often into vertical integration of varying degrees. If the Bank of England’s recession predictions come true, those relying on a percentage charge of assets might be forced to put new revenue-generating plans to the top of the to-do pile. The rising interest rates also means platform cash rates and how much is returned to clients is likely to come back under the microscope too.

Naturally, a recession is going to hit platform sales and inflation and the rising energy charge cap (which seems to serve less and less like a charges cap) in October and January means the rest of the year is going to be tough.

At least it’s hot, eh?

IT’S DANGEROUS TO GO ALONE, TAKE THESE! (LINKS)

- Our latest Podcat on Consumer Duty with Tom McPhail and Mike Barrett has proved essential listening according to our download stats. If you’ve not heard it yet, you can find it here.

- We’re continuing to grow the list of providers on our MPS section of Analyser. Here’s a few helpful videos to help you get the best out of it.

- Finally, here my music choice to help you along the way. It’s hot, so your movement should be slow and silky. To that end here’s a groove from fantastic UK reggae, dub, ska, punk band The Skints

Cheers,

Rich