By Rich Mayor and Natalie Holt

The direct-to-consumer market has tended to co-exist pretty happily alongside the advised market over recent years.

There will be times when different treatment between the two channels raises eyebrows, but largely the squabbles over providers attempting to ‘poach’ advised clients for their D2C business seem to be a thing of the past. D2C is catering to one market, and advice to another.

Or so the argument goes. Yet analysis as part of our latest State of the Platform Nation (SOTPN) report suggests a rise in the adoption of D2C platforms, both among new investors but also, anecdotally, among existing advised clients deciding to go their own way instead.

The warning signs are at an early stage, but they are there nonetheless. And if this trend continues, this could spell trouble both for the advised sector and the platforms that serve it.

D2C on the march

As part of SOTPN, we asked advice professionals what the driving factors behind client withdrawals were last year.

Beyond the nervousness created by the long wait for the Budget, some advisers pointed to an increasing desire among clients to self-manage their investments.

This comment stood out in particular:

“We did not see much outflow that was Budget-led; however the outflows we have seen in Q4 were more to DIY providers after several years of questioning the value of fees.

“We have had a real push in recent times to ensure what we offer aligns with Consumer Duty, however this was still not enough to retain some clients … lured by lower cost DIY platforms and increased confidence in self-management after a number of years of ongoing advice.”

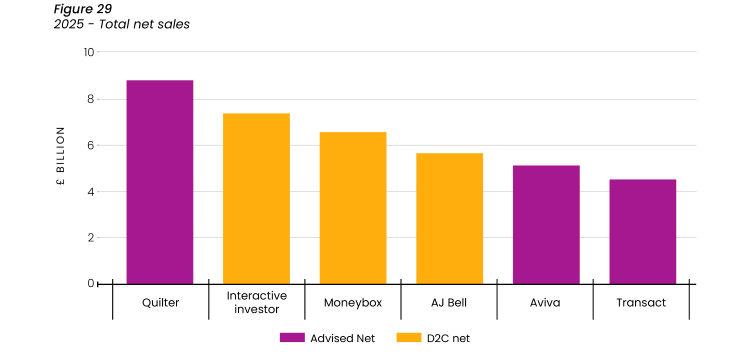

At the same time, it is interesting to see what the net sales figures for 2025 are telling us.

We can see here that three D2C platforms – interactive investor, Moneybox and AJ Bell – are posting huge net sales, in line with and sometimes surpassing the big advised platforms. (Hargreaves Lansdown, if you’re wondering, no longer publishes comparative data.)

In terms of total client numbers, interactive investor now has half a million clients, AJ Bell is close to that figure at the time of writing, and Moneybox’s latest accounts show it added nearly 400,000 customers in a year, and now has over 1.5m customers.

The Covid lockdown in 2020/21 encouraged those with disposable cash to invest, and that shift in investing behaviour seems to have taken hold. Rather than investing being a lockdown-induced ‘flash in the pan’, the knock-on impact seems to have been the creation of actual long-term investors.

So if the D2C market is growing at pace, what are the implications for advice and advised platforms?

The adviser backdrop

This emerging D2C trend comes at a time when things aren’t looking all that great in the world of advised platforms.

From a commercial point of view, advice firms are in a good place. Separate data from State of the Advice Nation shows a sector that’s pretty positive where outlooks on turnover and profit are concerned.

Yet other figures show there’s more going on. Data from the FCA on the shape of the advice market shows the number of advised clients has plateaued over the past couple of years.

As of 2024, the latest data available, there are around 3.5m advised clients. While the number of advisers is broadly stable at over 28,000, that will include those who are looking to retire in the near future.

Any clients that are lost to D2C will be replaced by new ones coming through the door which, while positive, doesn’t grow the number of clients being served.

There is also the fact that advice and planning business models are built on providing an ongoing service, funded by ongoing charges. The same FCA data tells us that over 80% of revenue comes from ongoing charges. If ongoing service and charges are reduced from where they are now, that has clear implications for advisers’ future revenues.

The advised platform perspective

Consolidation in the advice market means fewer advice firms to go around, and tends to result in firms adopting new platform panels as result. We see that reflected in advised platform flows over the past couple of years, with flows concentrated to just a handful of players.

The advised platform market is a mature one, now seeing high outflows. Investments are maturing, and new clients are needed to replace what’s going out.

As one advice professional told us:

“There’s already a lot of money on platforms, and some people are spending it.”

And that’s before we get to AI…

These shifts are likely being compounded by the use of AI.

Some consumers at least are happy to get their pension advice from AI, and we know from consumer research we’ve carried out with Royal London and YouGov that 23% of respondents are using AI-based services like ChatGPT and Microsoft Copilot to help manage their finances. This rises to 55% of consumers with an income of over £65,000, a cohort likely to benefit from the value of advice.

Those finding their way to investing directly may also be leaning on their AI tool of choice for researching D2C platform costs (despite probably being unable to compare the true total cost, as Mark wrote about recently here).

Reading the signs

Not all of this is within advised platforms’ control. But they can still mount a response if the shift to D2C persists.

Fees is an obvious lever, though it’s one that has probably already been pressed to a large extent on advised platform pricing. We may see fee pressure from investors and advised clients having a small effect on already squeezed platform margins.

For us though, the more fundamental question for advised platforms is what can you do to grow the advised client base you can compete in?

Record sales and positive markets have so far masked some big underlying issues within the advised platform market. But if we see sustained, poorer market conditions, and advised clients withdrawing more, be it to go D2C or simply to spend, the advised platform market could be in for something of a reckoning.

—

This article is based on an extract from State of the Platform Nation 2025/26, available to download now for adviser and provider subscribers via Analyser.

If you’re an advice professional wanting to get hold of SOTPN, it’s included as part of an annual Everything Analyser subscription. Find out more

If you’re a provider wanting to access the report, get in touch – your organisation may well have access already.